Before we move into this fortnight’s market update, let me start with some exciting breaking news.

Former Prime Minister John Howard has confirmed he will be joining us as keynote speaker at our upcoming Business Meet Sports Lunch, taking place on 20 March at The Star, Gold Coast.

I’ll have the privilege of interviewing Mr Howard, exploring his journey from his early years through to the experiences that shaped his leadership, along with his perspective on the challenges and opportunities facing Australia and the world today. He is widely regarded as one of the most thoughtful and influential political leaders of modern times, and I expect this to be an extraordinary conversation.

The sporting component of the lunch will feature the Gold Coast Titans, who are entering an exciting new chapter. With fresh additions to the ownership group alongside Brett and Rebecca Frizelle, plus well-known rugby league personalities including Gordon Tallis and Matthew Johns, together with new Head Coach Josh Hannay, the discussion promises to be both insightful and entertaining.

I strongly encourage you to secure your table early via www.rwbellgroupevents.com

This event will sell quickly and is shaping up to be one of the standout business and community gatherings of the year.

Across the broader market, the consistent observation from industry participants, business leaders and consumers alike is that 2026 has commenced with considerable momentum. Activity levels remain high across multiple sectors despite ongoing economic commentary urging caution.

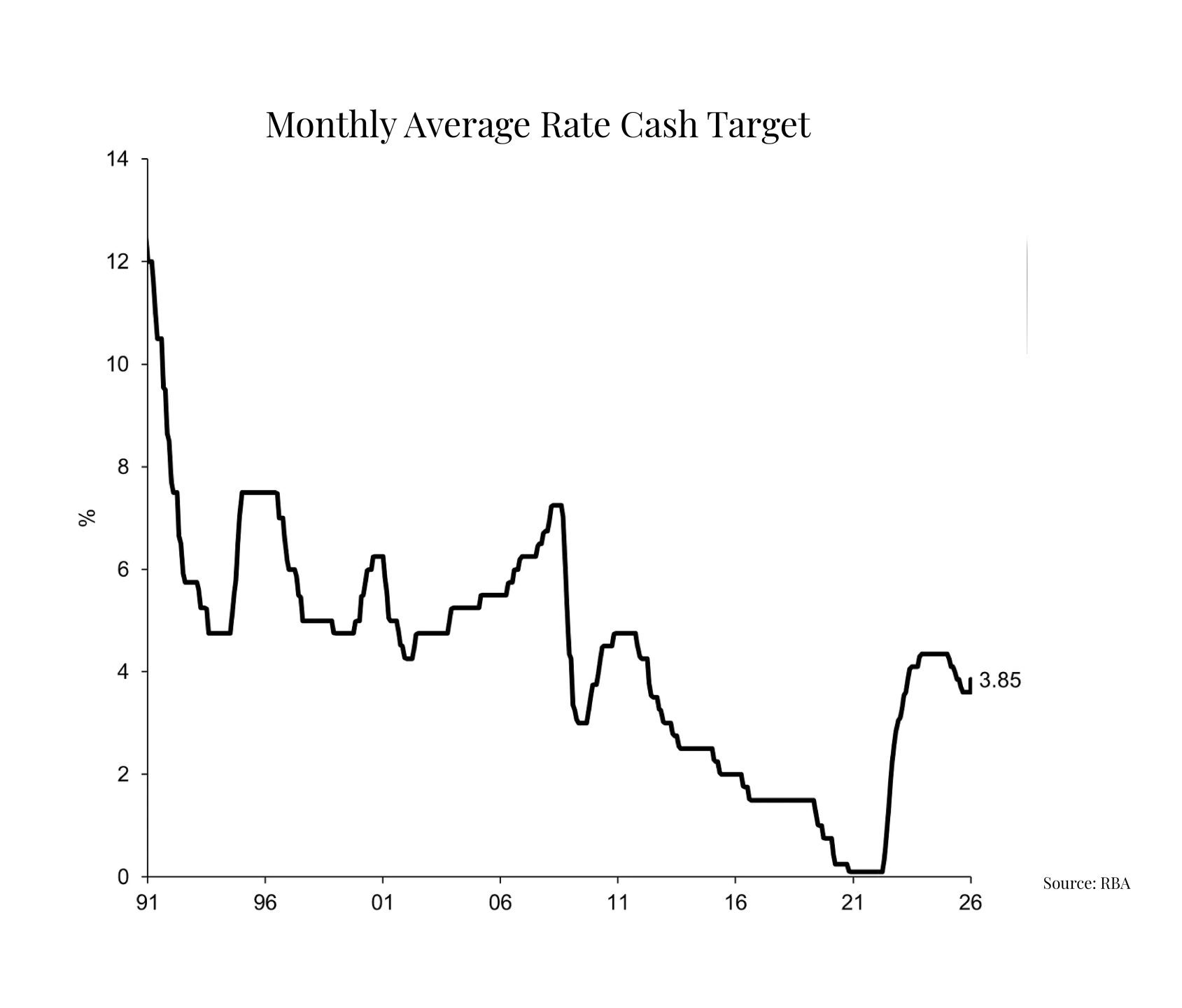

The first inflation figures for the year recorded a reading of 3.8 per cent, prompting the Reserve Bank to implement a 0.25 per cent interest rate increase. The decision was largely anticipated, reflecting the Bank’s continued mandate to return inflation to its target range of between two and three per cent. Interest rates remain the central mechanism through which inflationary pressures are moderated, particularly those linked to labour costs, materials pricing and production expenses.

While a single rate adjustment rarely produces immediate behavioural change, historical patterns suggest the Reserve Bank seldom moves only once. Further increases remain possible later in the year. Housing costs continue to represent the largest contributor to inflation, currently growing at approximately 5.5 per cent annually, driven primarily by rental growth, construction expenses and energy pricing. Importantly, these pressures are largely supply-driven rather than demand-led.

Market participants frequently seek definitive forecasts for the year ahead; however, certainty is rarely available in property markets. What history consistently demonstrates is that interest rate increases do not automatically translate into reduced activity. In many instances, the opposite occurs in the short term, as buyers accelerate decisions to secure finance positions ahead of potential future rises.

Recent auction results provide a clear example. At Ray White Bell Group’s auction of 34 Rio Vista Boulevard, Broadbeach Waters, held shortly after the latest rate increase, twenty registered bidders competed in front of an audience approaching one hundred attendees. The property ultimately sold under the hammer for $2.41 million, achieving a result approximately twenty per cent above reserve. Such outcomes reinforce the continued depth of buyer engagement despite changing financial conditions.

(Comparison of Interest Rates Over the Past 30 Years)

Longer-term perspective remains important. Australian property markets have historically performed strongly during periods of significantly higher interest rates than those experienced today. During the 1990s, markets operated successfully with rates approaching eighteen per cent. While modern cost-of-living pressures make contemporary markets more sensitive to monetary policy movements, higher interest rates alone do not determine market strength.

The underlying structural issue continues to be supply. Australia is not producing sufficient housing to meet ongoing population growth, while many existing property owners are choosing to retain assets rather than sell. This constrained supply environment continues to support demand fundamentals across the residential market.

The primary effect of rising interest rates is less about repayment stress and more about borrowing capacity. Each rate increase can reduce average borrowing power by approximately $15,000, meaning multiple adjustments throughout the year may cumulatively limit purchasing budgets. This gradual reduction in capacity typically moderates price growth rather than abruptly reversing market conditions.

Global influences remain the principal wildcard. Geopolitical tensions, trade uncertainty and broader international economic conditions all have the potential to influence confidence levels. Even allowing for these variables, the Gold Coast market appears positioned to continue performing strongly, albeit at a more measured and sustainable pace following five years of exceptional growth. Such moderation would represent a healthy phase of market normalisation rather than weakness.

Final reminders remain for the upcoming Business Meet Sports Lunch, which brings together business leadership, sport and community engagement in one of the region’s most anticipated networking events. With John Howard joining representatives from the Gold Coast Titans, the afternoon promises meaningful discussion, valuable connections and significant insight for the broader business community.